"Cost-Effective" is a Coalition euphemism for "Cheap and nasty". What it hides is a business that is

meant to never pay for itself, let alone

ever make a return. At best, FTTN lines will make

$48/yr/service while NBN Co is already making

$218/yr/service,

450% higher income.The worst case, and highly likely, is for Telstra payments to cause

FTTN services to lose $100/yr.Business Owners understand there are

two sides to the ledger:

Costs and Revenues.

It not Good Business to reduce Costs if that destroys, as the Coalition does, your ability to raise Revenue.

Is installing 68,000 nodes then haphazardly running the

odd fibre from those forlorn, stranded boxes to desperate, frustrated customers "Cost-Effective"?

A quick analysis suggests it will be an expensive failure and those foolish to pay the "Earls Ransom",

will not get the near the same service as direct Fibre subscribers.

Below I

borrow from a longer piece, a comparison of Copper and Fibre Costs.

To that, add the unacknowledged Elephant in the Room:

Payments to Telstra - $30-$180/yr/active service.

Because bits are agnostic about how they're transmitted, I'll omit Volume charges. We can expect them to be identical for users with the same access rate, regardless of connection type.

I've also omitted overhead charges, which I could guess at 25% of other costs, but which will be similar and I have no sound figures to estimate from.

From Coalition estimates, a DSL line will cost $162/yr to run and earn, at most, $240, a margin of $78, excluding payments to Telstra.

The

best outcome after Telstra payments, would be

$48, the worst, and more likely, outcome a

loss of

$100/line/yr.

Compare that to fibre, with a current surplus of

$218.

Current income of $360/yr/service for access only.

And costs of $112/yr plus $30/yr to Telstra for $142/yr.

Margin without overheads = $360 - $142 =

$218.

This ignores the

intended losses in

Throwing away the FTTN Network and also having to still pay the

currently contracted Telstra payment to buy the lead-in and compensate for loss of the Phone Service.

Real Copper and Fibre Revenue

The 2014 Coalition forecast [pg 31 & 21 of

Background doc] for ARPU is $22.26 vs the NBN Co Plan of $31.10,

a 28% reduction. [ARPU = Average Revenue Per User, or Total Revenue divided by Users,

per month].

To achieve the $22.26 figure, 10% lower than the $31.10 NBN Co Plan including Volume charges, they must charge under the current minimum AVC charge of $24 for all services. The Coalition can only be charging $18-$20 for FTTN access. But they've never revealed their AVC for FTTN services used in their modelling.

In April, the CEO of NBN Co, Mike Quigley, informed the Parliamentary Committee that the current ARPU was $38, close to the 2015 forecast figure and 33% ahead of the 2013 forecast.

From the NBN Co Rate Card for AVC's and the figures published in April of take-up rates by plan, the access charge is averaging $30/mth, or yearly income of $360.

Comparing Copper and Fibre CostsNBN Co in April released construction figures for direct Fibre: $1100-$1400 per service. These are commercially supported figures, not estimates or guesses based on dissimilar projects.

The Coalition detailed plan suggests they used $900/service passed for VDSL2/FTTN (Copper) with $90/service in line-related maintenance, 10% of the capital price.

NBN Co have not released figures for line-related maintenance. Elsewhere there are suggestions Fibre is 7-8 times cheaper to maintain than FTTN. The Coalition suggested a figure of 1.5-2% of capital cost, this would be $20-$25/service.

The Depreciation rates of the two networks, FTTN and FTTP, Copper and Fibre, are different, but with their different build cost, they end up depreciating around the same amount per year.

The Copper Network will have a service life of 15-20 years, while the Fibre Network will have more than 30 years in service.

Copper depreciation per service, straight-line, will be $900 ÷ 20, or $45/year,

while Fibre depreciation per service, is $1400 ÷ 30, or $45/year.

According to reliable commercial figures, the FTTP (Fibre) network is only 50% more than the price guessed by the Coalition. At 3% p.a. interest, that's $27 for Copper and $42 for Fibre.

Total Costs (Interest, Depreciation, Maintenance) per service are:

Copper = $27 + $45 + $90 = $162

Fibre = $42 + $45 + $25 = $112.

A Fibre Network will be $50/year/service

cheaper to own, around 30% less based on

sound figures.

Comparing Copper and Fibre Network chargesThere is a small variable cost in CAN's related to cost-per-bit. Consumers value services based on what 'utility' it provide them. For someone

that has a need, higher access rates are worth more.

While access-rate barely affects costs, it can be used to differentiate services for users. For Fibre here are 3 indicative prices: 12/1Mbps: $24, 100/40Mbps: $38, 1000/400: $150. For users that need higher speeds, they offer exceptional value. To the consumer, it's

twenty times cheaper to buy a single 1000/400 Mbps service than 80 of the slowest services.

Currently, the access charges of NBN Co average around $30/user. That's a 25% increase for

exactly the same physical equipment,

just for asking. You'll find customers buying the premium service are

extremely happy with the deal.

When 1000/400 Mbps access is offered, the average will kick up by another 15%,

just for asking. And underlying the point, with customers happy

they are getting an outstanding deal.

For a Copper CAN, without the ability to guarantee

per-customer access rate, a single access price of $20-$24 is all that could be charged, the same or less than the cheapest rate for Fibre. It may be possible to increase charges for VDSL2 and VDSL2 Vectoring services, but probably only by 10%.

Right now Fibre Access earns 50% more than Copper, with a 15% kick coming soon.

Comparing Copper and Fibre Revenue GrowthWhile a Fibre CAN (FTTP) is 30% cheaper to run than a Copper CAN (FTTN) and currently gets 50% higher access revenues than Copper by delivering

guaranteed access rates, the

1,000-fold less cost-per-bit means

nothing, if there is

no demand. I contend that Fibre, and only Fibre, unlocks the economic potential of Customer Data Networks because of tiered pricing, with high-end users self-identifying and being charged a premium for access and volume by RSP's.

This is where the Customer Demand Distribution comes into play. Sandvine data,

for the USA, 1H 2013, show the low 50% of consumers account for just 6.4% of traffic. If you dropped them off the network, download volume would barely change and ARPU, Average Revenue Per User (per month), would increase considerably because there's a link between higher line access rates and higher downloads.

People with a need for speed, download and upload more.

The high-end 50% of users account for around 95% of total traffic, more for upload. The top 1% of users consume 10% of total traffic. These are the people driving demand and traffic growth.

Data Networks for Customer Access are

not built for the average user, t

hey account for an insignificant volume of traffic. The customers that drive demand and fill your order books are the top 1-10% of users.

People who base their argument on "I don't need more speed, therefore the whole thing is a waste of time and money", don't understand the economics. They are almost noise in the system.

The long-term

average download demand reported by the ABS has grown at around 70% (1.3 year doubling period) for some time, despite the average line access rate being limited to 4.2Mbps. We

know that 95% of this traffic is from the high-end users:

the ABS data is a good description of the solid, exponential-growth of demand by the early adopters. It is

not a measure of ordinary use.

Network Operators will make their money from the top 1-10% of customers who will both buy the highest offered line access speeds and generate the bulk of the traffic. These customers can be charged a premium for both access and volume ($/GB) by RSP's - they have shown a willingness to pay and the NBN Co pricing model encourages this.

Low-end users, the late-maturity and laggards in market-speak, will either continue their current usage patterns and enjoy continually falling prices, or increase their usage for roughly constant ARPU.

Some will discover their unique "killer application" and move up the curve above the 50th percentile.

For a Fibre network, the demand for increased volume and access rates will continue, because it is driven by the top 50% of users, especially the top 1%-10%, and the last 15 years of data tells us they are following the six decade old Computing demand curve:

the thirst for data keeps growing as more is provided. [See

Bell's Law diagram of prices in

this previous post.]

Just as the business model of every Telco offering Telephone services is based on the

human characteristic, "

people love to talk", Computing devices and Data Networks are driven by a similar so-far insatiable human appetite for information and understanding: "

people want to know, 'Why?'". This same appetite drives the entertainment and education industries.

For a Copper Network, line access rate

cannot be guaranteed. Because of this, the most demanding users, the top 1%-10%

cannot be supplied with Copper services they'll pay a premium for:

supply and demand cannot be matched, a fundamental market failure.

Because all users will be charged a single price, RSP's will find it very difficult to charge a premium to high-end users, drying up their revenues.

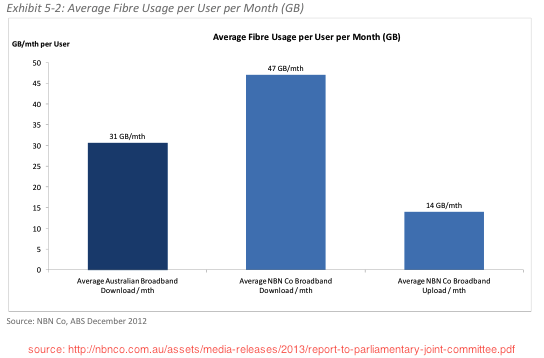

We know from the faster take-up rates of high-end Fibre services and that average monthly downloads are

50% higher on new Fibre services, comparing to the Australian average, that there is significant pent-up demand in the Data Networking market, especially in the important and highly profitable high-end.

This pent-up demand cannot be reliably served or exploited in a Copper network because high-end users cannot reliably be matched to faster services.

As well, there's barely

any speed increase options available, and they are increasingly expensive to deploy, versus the exponentially dropping cost-per-bit of Fibre transceivers.

Copper is being pushed from two ends:

slower and 1,000 times more expensive!

{kind=link}