If you missed Part1 you can see it here.

QoS (Network Quality of Service)

QoS refers to the how data packets are sent through networks: which go first, which wait and which get thrown away. The aim of this is to give better delivery times for specific types of traffic like voice or video streaming. QoS is not a "guarantee", only a priority. The implementation of QoS with copper line ADSL networks is about guaranteeing transmission rates, error rates and other specific characteristics of network traffic. Simon asserts that with using fibre all the way to the premise (FTTH/FTTP) the abundance of bandwidth in the GPON renders QoS pointless.

Simon's criticism is correct and valid, paraphrased as: "Within the NBN CAN (Customer Access Network) there is no need for QoS prioritisation, because there should never be significant congestion and queues to address." Yes, and that is what the NBN Co docs say they'll do.

NBN Co make it clear that they add QoS 'tags' to customer packets at source (the NTD), not for their network, but for the RSP's. QoS is to allow the RSP to buy smaller CVC's (pay less), smaller backhaul (pay less), creating some congestion/queuing in peak-times whilst being able to trivially provide different grades of service to customers (charge more).

QoS and packet prioritisation is solely there for the benefit of RSP's. They get to minimise costs and increase their revenues. If I was an ISP, I wouldn't argue against it... QoS puts in place a means to ensure good performance of critical services into the future, thereby guaranteeing consistency to all parties.

With slower and more unreliable DSL networks, QoS is much more important for time-critical services, like voice & video streaming, on Copper Networks (FTTN).

Tiered AVC Charges & lower CVC (Volume) Charging

NBN Co sells wholesale services only. These services are purchased by Retail Service Providers (RSP's) who then offer access services to individual customers. To identify their traffic within the NBN, each RSP purchases an "Access Virtual Circuit" (AVC). RSP's generally purchase one AVC per customer. NBN Co is charging these AVC's out in multiple 'speed tiers', where the faster the speed supplied, the higher the charge.

Multiple AVC is a brilliant commercial innovation on the part of NBN Co, soundly based in Economic Theory and of real value to RSP's: they can charge different clients more for exactly the same physical service.

Look at Exhibit 8.5 of the NBN Co Plan: they charge between $24 (12/1) and $150 (1000/400) for the same physical line. The RSP can just add their margin, or charge a premium for higher speeds, and the presumed higher downloads that go along with it. Like iiNet, they can raise the per-GB price of included data for 'premium' plans.

In Economics, this is called reducing Consumer Surplus, or "not leaving money on the table". Nobody is forced to pay higher AVC charges. Customers are able to put a dollar figure on what the extra access rate is worth, to them. Providing customers with a choice of models, to express their preferences and willingness to pay, is fundamental to the consumer goods business. It's great business to abandon the current ADSL single-fee model.

But it doesn't stop there: NBN Co will reduce the AVC charges over time. By 69% for 100/40 and 82% for 1000/400 in 2040 (nominal, not real $). [Exhibits 3-1 to 3-3 of April 2013 and Ex. 8.8 of 2012 Plan]

And it gets better: The NBN comprises multiple "Connectivity Serving Areas", each with a PoI (Point Of Interconnect) where RSP's connect their backhaul links. RSP's purchase a CVC (Connectivity Virtual Circuit) at each PoI they wish to serve. The CVC is a pipe, the size (bandwidth) determined by the price ($20 per 1Mbps).

NBN Co will reduce CVC charges as average monthly volume increases, not total volume. [Exhibit 8.9 of 2012 Plan]. RSP input costs from NBN Co will halve after 3-4 doublings in traffic. At current rates of growth, that's before 2020.

What Simon didn't raise is that the willingness of consumers to buy premium plans is higher than the rate NBN Co reduces prices (32% @ 100/40 not 18%), prompting them to bring forward higher rate plans (read more profitable) up to 1000/40. [Exhibit 4.3, April 2013]

This benefits RSP's as much, or more, than it benefits NBN Co. They not only increase revenues, they can increase their Gross Margin (EBITDA) as well: consumers are showing their willingness to pay a premium. Building on that is good commercial practice.

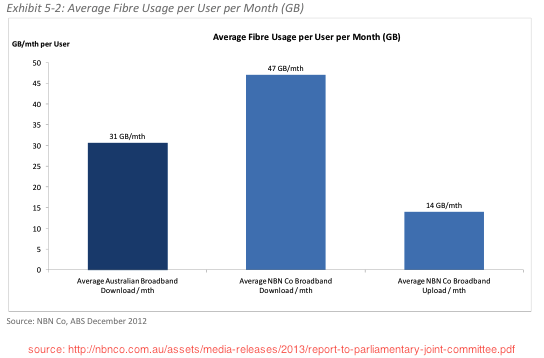

Not only have take-up rates and high-end AVC's exceeded forecasts, but average download volume is 50% higher than the Australian average (45GB/mth vs 30GB/mth) [Exhibit 5.2, April 2013]. That's more revenue and potentially higher Gross Margins for RSP's as well. Exhibit 5.1 [April 2013] shows that fixed-line download volumes are growing solidly and at much higher rates than mobile data: Fixed-line is where the money is to be made.

Exhibit 7.6 [2012 Plan] shows that independent experts are forecasting this continuing exponential growth in demand to continue well past 2040. [That's a log-scale, not linear, of speed. Even line is ten-times more than the last.]

Could it get any better? I think so...

The high take-up rates of 100/400 [Ex 4.3, April 2013] coincide with the Sandvine traffic distribution graph [final graph]: 1% of users account for 10% of traffic, while the lowest 50% of users account for 6.4% of traffic.

If the overwhelming majority (~95%) of your demand is from high-end customers, who self-select their willingness to pay a premium and on which you can make higher Gross Margins, do you throw away that business and ignore the premiums? No, it's not good business.

RSP's can afford to lose 50% of their customers, the low-end, to mobile competitors and it will increase both their ARPU's and their Gross Margins. I don't have the data to say if demand growth rate will increase as well.

In answer to Simon: NBN Co has already given RSP's decreasing volume charges, but has also gifted them increased revenue (tiered AVC's) and allowed them to differentiate premium customers and increase Gross Margins. Neither of those are available, or possible, under a single-rate DSL/FTTN regime.

This commercial strategy of introducing premium products at high Gross Margins, then steadily reducing the price and Margin as new higher-spec/feature products are released over them is well established. It's the enormously successful Apple Strategy.

Charts [click to enlarge]

|

| Simon's calculated ARPU |

|

| NBN Co 2012 Plan |

|

| NBN Co 2012 Plan |

|

| NBN Co April 2013 |

|

| NBN Co April 2103 |

|

| NBN Co April 2103 |

|

| NBN Co April 2013 |

|

| NBN Co April 2103 |

|

| NBN Co April 2103 |

|

| NBN Co 2012 Plan |

|

| NBN Co 2012 Plan |

|

| NBN Co 2012 Plan |

|

| NBN Co 2012 Plan |

|

| NBN Co 2012 Plan |

|

| Sandvine, 1H 2013 |

Sources

April, 2013, NBN Co report to Joint Parliamentary Committee

http://nbnco.com.au/assets/media-releases/2013/report-to-parliamentary-joint-committee.pdf

Aug, 2012, NBN Co Corporate Plan

Sandvine Global Internet Phenomena, 1st half, 2013 [Graph for North America]

No comments:

Post a Comment

Note: only a member of this blog may post a comment.